Here we’ll review the basic structure of a typical investment fund. This setup works for funds of all asset classes (venture, real estate private equity, crypto, etc.). Both closed-end and open-end investment funds can use this structure.

Here’s a link to the full-sized investment fund structure chart.

{kind=link}

Who are the parties in an investment fund?

On a high level, investment funds typically have two main parties:

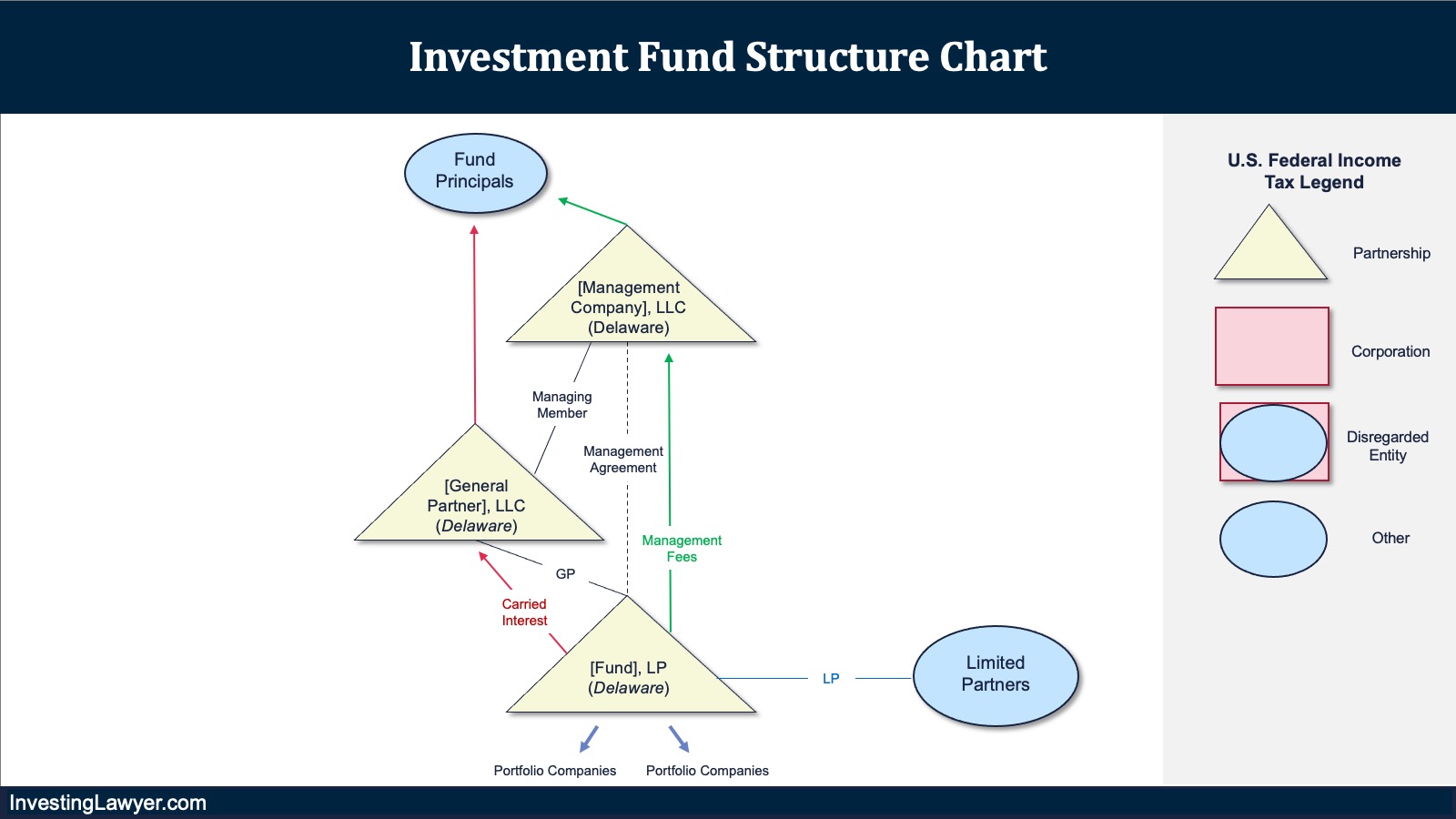

- Limited Partners (LPs) are the fund’s passive investors. They provide capital but don’t manage the fund or its investments.

- General Partners (GPs) run the show. While the general partner often invests in the fund alongside limited partners, the general partner’s main job is to identify, purchase, manage, and sell investments. You might also hear the general partner referred to as the “sponsor,” “manager,” “managing member,” or all sorts of other things. The exact name often depends on the fund’s legal structure but they’re all basically synonyms. The individuals running the sponsor are often called the “principals.”

How is the sponsor of an investment fund paid?

Sponsors usually get paid in two main ways:

- Management Fee: Most funds pay the sponsor a fixed fee calculated as a percentage of the fund size.

- The standard management fee is 2% per year. So for a $100M fund, the management fee would be $2 million annually.

- The fund’s asset class affects the details of how this fee is calculated. For example, after the fund’s investment period ends, most venture capital funds start reducing the management fee’s percentage each year (1.9%. 1.8%, 1.7%, etc.), while most private equity funds switch the fee from 2% of the fund size to 2% of capital actually invested (reduced by any investments that have been sold or written off).

- Here is a more detailed description of the management fee (and other fees) in real estate funds and syndications.

- Carried Interest: The fund also pays the sponsor a share of the fund’s profits, which is called the “carried interest” or the “incentive distribution.”

- The standard carried interest is 20% of the fund’s profits. So if limited partners invested $100M and after selling all the fund’s assets the fund has $200M left, the first $100M goes to the limited partners to return their capital and the remaining $100M are the “profits.” The remaining $100M would be split $80M to LPs and $20M to the GP.

- Often the carried interest calculations can get complicated and include concepts like preferred returns, GP catchups, and deal-by-deal waterfalls. We’ll discuss these concepts in future articles.

- Here is a more detailed description of the carried interest in real estate funds and syndications.

The three main investment fund legal entities

Most sponsors will form three legal entities (usually in Delaware):

- Fund. This is the fund itself. This is the entity that limited partners will invest in and the entity that will invest in companies, real estate, crypto, etc.

- General Partner. This is the official “general partner” entity with legal control of the fund. The general partner entity typically receives the carried interest. A new general partner entity is typically formed each time a sponsor forms a new fund. So if a sponsor has four funds, they’ll have four general partner entities as well.

- Management Company. Most sponsors form a third entity called the “management company.” The general partner entity typically enters into a “management agreement” with the management company where the general partner delegates some of its duties to the management company. In return, the management company gets the management fee that the general partner would have otherwise received. Most sponsors form just one management company, which receives the management fees from all funds formed by the sponsor. In most funds we set up, the management company legally controls the general partner as its managing member, but this isn’t required.

Other ways to structure an investment fund

For tax and regulatory reasons, many investment funds are structured in much more complicated ways and include additional features such as:

- Feeder funds

- Parallel funds

- Blockers

We’ll get into these concepts in future articles.

For more information about the timeline and process of forming an investment fund, check out our investment fund formation timeline.

Thank you – a clear overview that is easy to read and understand for those new to the field

Thanks for reading!